Once upon a time, in a land far away, people first began to congregate in the dusty streets of ancient cities to trade goods and information amongst themselves and their fellow citizens for the benefit of all mankind. And they kept doing it the same way for the next 5,000 years. The end.

Well kind of.

Markets have existed for as long as humans have engaged in trade. But the earliest bazaars – what we would recognise today as marketplaces – originated in Persia around 3,000 BC, and were focused on trading commodities like food, clothing, and basic household items. Competition was (almost literally) cutthroat, with tens or even hundreds of traders keeping an eagle eye on the offerings of others, and being prepared to undermine their prices to get the sale at any cost.

Disruption in these markets was driven by novelty - shiny objects like precious metals, aromatic spices, and exotic materials brought in by merchants and travellers from distant regions and countries. A savvy market trader could hope to keep ahead of the competition by having a steady flow of new and different things to attract the eye of their passing customers.

But even the most inventive market trader eventually comes face-to-face with the reality of commoditisation – that exasperating point in the maturity of any market where it seems everyone is selling the same shiny objects for ever cheaper prices. We all know a race to the bottom simply isn’t sustainable (don’t we?), so smart traders learned to differentiate by getting to know their customers and catering to their individual needs – understanding how and when to put the right product in the right place at the right price with the right promotion to get people to part with their hard-earned cash.

Fast forward to the 21st century, and much of how we do business today hasn’t changed. What has changed dramatically is the scale of the businesses that operate in increasingly globalised markets, and the leverage that these companies have in governing many aspects of the way we experience the world by interacting with them. What has also changed is the agility of businesses in recognising and responding to social and economic change which is happening around them.

The truth is, when left to their own devices, established businesses in the same vertical market do not tend to disrupt themselves. As we discussed in our opening article in this blog series about Digital Disruption: it simply isn’t in our DNA anymore.

Especially in the world of telecommunications, we’ve forgotten the basics of trading in open competition. And as a result, behaviour patterns creep in which look to the objective outside observer like, well…cartelism. Competition stagnates. Price changes are coordinated or become a game of rapidly-following-my-leader. Complacency sets in, and consumer choice suffers.

In many national telco markets around the world there appears to be a tacit agreement amongst market leaders that they have carved up the market in a certain way over time. And this is just the way things are now. It’s just obvious. Right?

Wrong.

History teaches us that at this point of maximum complacency – when the pieces on the board are set a certain way, when things are at their most “obvious” – traditional players in established markets are at their most vulnerable to disruptive change. Here are just a few examples of this you might recognise in the real world:

- Before 2003 it was “obvious” that if you wanted a new car, you got either a petrol or diesel vehicle from one of 5-6 global conglomerates. And if you wanted an upgrade, you bought a new model.

Then Tesla came along and disrupted the market with all electric cars that could be upgraded on the fly, and offered a superior buying, owning and lifestyle experience to any of the conventional alternatives. - Before 2009 it was “obvious” that if you wanted to book a taxi you either hailed one on the street, or called a number to pre-book, and rolled the dice on the quality of ride you were getting into and whether the driver knew how to get to your destination –or even where to pick you up. And of course you had to make sure you had cash in your pocket.

Then Uber came along and disrupted the market with a simple easy to use app, that offered a simple way of locating yourself the nearest ride, in a new clean car, with a driver that had a GPS-equipped map to your destination, and your payment was taken automatically from your card. - Before 2015 it was “obvious” that if you wanted to open a bank account or get a payment card you went to a branch of an established high-street bank between the hours of 9am – 3pm Mon-Fri, had an interview with a clerk, filled in a lot of paperwork, handed over a lot of documentation and maybe got your new cheque book or debit card delivered to you a week later.

Then Revolut came along and disrupted the market by allowing you to sign up using Digital identity verification in the comfort of your own home, or in a restaurant or a football stadium (you get the idea) and have access to a virtual card and bank account within 5 minutes. Your physical card arrives the next day.

For a really vivid example of how quickly things can change in one area of our own industry take a look at this astonishing visualisation from James Eagle, of EEGALI, which shows how dramatically and completely the mobile handset market has been disrupted in the last 30 years – look how “obvious” it was before 2007 that you got your phone from either Nokia or Motorola (or Blackberry – remember them??).

CLICK IMAGE TO PLAY VIDEO

https://www.youtube.com/watch?v=VgBdaVegxUA

(This video has a cool soundtrack – if you want to listen to it, do so with the volume up. If you don’t, you have been warned!)

In the Digital economy these disruptive pressures are compounded. Disruptive influences are no-longer limited to the narrow focus of individual vertical markets. New ideas are being born in one vertical and cross-pollinated or reimagined in others on a constant basis and at a rate we have never experienced before.

Banking businesses are stealing with pride from Entertainment businesses, who are stealing with pride from Gaming businesses, who are stealing with pride from Social Media businesses. And Digital hyper-scalers are striding across industries like the giants of ancient fairy tales, their well-fed magic geese laying the golden eggs of structural disruption as they go.

What is becoming clear, is that the value equation in the telecommunications industry needs to change if we are to succeed in the Digital economy. Service providers are no longer competing for the “connectivity dollar” that they were 15 years ago. They are competing for the “lifestyle dollar” of increasingly discerning consumers who expect things to be done in a highly personalised way on their terms.

We shouldn’t be obsessing over prepaid vs postpaid subscriber definitions any more than the car industry should be obsessing over who buys petrol vs diesel engines. These are legacy artefacts of a bygone age. We also need to resist our urge to “define the market” in terms of large homogenous - and largely fictitious - segments layered by price sensitivity. Digital consumers don’t care about such things and defy compartmentalisation in a way that we are not used to in our industry.

It takes a truly enlightened telco marketing executive to realise and accept that we don’t own or control the consumer in this new business model anymore. Instead of trying to shoehorn this new reality into our old ways of thinking, we should get busy learning how to deliver value to individual customers in a quick, convenient and transparent way that suits their needs. And – perhaps more importantly than ever – matches their values, and the values of their peer groups and communities.

The apps and services that get this right will get the attention. They will get the downloads. They will get the engagement. And, ultimately, they will get the money. Those who don’t embrace this fundamental change in expectation and behaviour - or don’t find innovative ways to continue to stay relevant - will fall quickly by the wayside, and the fairy tale will change into a nightmare.

If you want to get defensive about this challenge, then sure: you could argue the barriers to entry in the traditional telco industry remain high – few companies have the billion-dollar budgets to build networks or the political clout to win licences to operate them. So who cares? Who’s going to challenge us? But make no mistake: the barriers to exit for a telco consumer – and certainly the barriers to complaining loudly and visibly in a very public way – have never been lower. You ignore this paradigm shift at your peril. Because the barriers to failure as a service provider are almost non-existent once discerning Digital consumers decide to turn their backs on you.

To stay relevant in the Digital economy, and create value at scale, telco marketing executives must go back to the trading basics born in those dusty bazaars on the streets of ancient Persia. Digital technology gives us orders of magnitude more insight into individual likes/dislikes/habits than those archetypal market traders could ever have dreamed of.

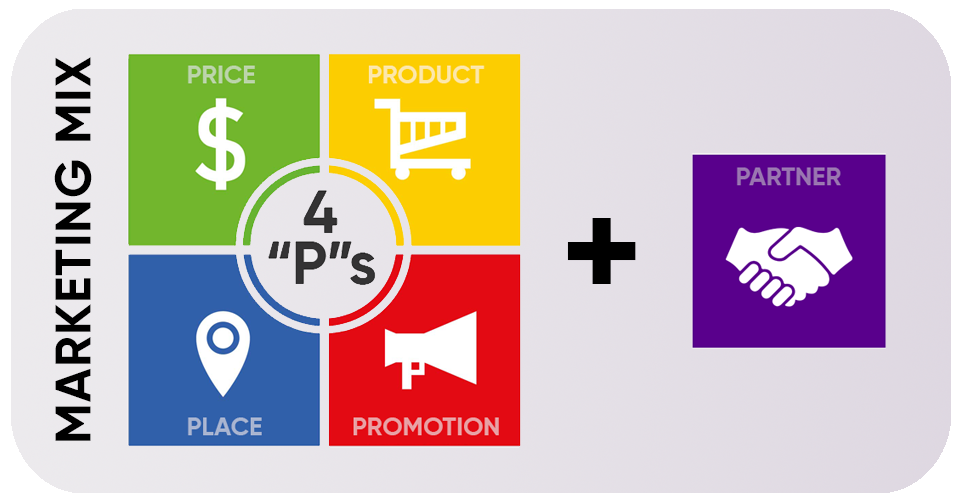

But we need to get back into the habit of leveraging these insights in the right way – to use the lakes of data we have at our fingertips to get to know our new generation of Digital consumers. We must get back to the basics of the 4 “P”s (Product, Place, Price, Promotion) of the marketing mix that our trading ancestors understood so well, and use them in combination with scalable automation tools to deliver highly personalised experiences to each individual customer. The alluring “segment of one” has never been more achievable.

Digital also demands that we look at adjacent opportunities outside of our core market to retain the interest of our customers and to keep us relevant in their busy Digital lives.

This introduces an important 5th “P” into the marketing mix in the form of Partners. Modern telco executives must become adept at using Partner ecosystems as a lever to create an enticing and evolving proposition that is sticky enough to keep customers coming back – after all the search for novelty is hard wired into the human mind, and once the dragon is awake it must continue to be fed.

If we can tap into the right approach for serving the search for shiny objects and continue to disrupt our own thinking about how we do so, then we have an opportunity to avoid complacency and falling foul of the external disruptors of the future. With the right marketing mix, and the right customer experience to deliver it, we can survive and thrive in the Digital economy.

Which brings us on to the next chapter in our tale of Digital Disruption, and how you make your customers’ experience of your telco business compelling and exciting in a way that is familiar from Digital services in other verticals. Because in this fickle world of distracting shiny objects, experience is everything.

But that, dear reader, is a story for another time…

One last thing…

Disrupting the telco market in your geography might feel like a long and difficult journey ahead. But no challenge is insurmountable, and as with any journey of meaningful change the key thing is to put one foot in front of the other and get started.

There is already a small but growing list of telco service providers who have taken the first steps to disrupting their markets with an All Digital proposition that embraces the principles I’ve discussed here. And Moflix is keeping track of who the members of this exclusive All Digital Club are so we can collectively learn from their pioneering efforts.

Maybe this blog post won’t directly inspire you to go out and change the world, but I’m hoping you will at least take some inspiration from those who already are. And when you’re ready to join them on the road to Digital success, just get in touch by pressing the magic button below.

We’re here to help.

This is Part 2 of a 10 part series on digital disruption in the telecommuncation industry. We will update the links as the new content is published.

I. Telco Disruption Introduction: "Disrupt or Die. The Digital Clock is Ticking"

II. Disruption of Markets: "Are You Sitting Comfortably? Then It's Time to Get Disrupted!"

IV. Disruption of Operating Models: Smooth Operator - Embrace Minimum Waste & Maximum Joy!

V. Disruption of Culture

VI. Disruption of Success Metrics

VII. Disruption of Working Practices

VIII. Disruption of Solution Architectures

IX. Disruption of Technology Assumptions

X. Disruption of Procurement Approach